Microsoft Excel was released in 1985 and has grown to become arguably the most important computer program in workplaces around the world. Its either quite amazing or ridiculous that we are still using the same programme and after three decades begging the question has nothing changed?

In business, any function in any industry can benefit from Microsoft Excel ‘MS Excel’, it is a powerful tool that has become entrenched in business processes worldwide—whether for analyzing stocks or issuers, budgeting, or organizing client sales lists and even fulfilling regulatory requirements such as shareholding disclosure!

The question is can this go on?

Many users are inherently ignoring the risks and depend on the aged application. MS Excel is primarily a data wrangling tool for many businesses, even sophisticated financial services companies are utilizing spreadsheets too.

In the world of rising regulatory demands, an important area of operations, namely ‘Middle Office’ is where the Risk and Compliance processing happens and its important to get it right.

The dependency by Middle Office on Excel is alarming due to the lack of alternative technology to fulfil regulatory disclosures especially when it comes to aggregating and calculating ‘figures’.

In the case of Shareholding Disclosures (SD), positions require daily monitoring and adhering to specified regulatory thresholds. If they should breach these thresholds it is the organization’s responsibility to provide those respective position details and submit this on a mandatory form to regulators globally – on-time and accurately.

Failing to disclose, one is deemed non-compliant and the organization or individual (very exclusive to SD and unbeknown to many that the responsible officer can be found liable and face fines even face imprisonment should they be found non-compliant).

IS YOUR RELIANCE ON EXCEL SUBSTANTIATED AND A RISK? THE ANSWER IS YES AND THERE ARE REALLY TWO GLARINGLY POINTS WHY THIS IS TRUE BEFORE WE ADDRESS THE FUNCTIONAL LIMITATIONS OF EXCEL ITSELF.

Firstly, EXCEL IS INAUDITABLE in that it is difficult to track use and activity. Isn’t risk and compliance process meant to be auditable to prove there is processes in place? Clearly the argument breaks down straight away. The dependency is because of the lack of alternatives and the resistance from employees with their comfort for this tool that they are reluctant to give this up. Thus it remains embedded in the Risk and Compliance processes. We know it’s a tool relied upon for the many banking workflows (front office less so, whereas for the middle/back office dependency is high). The audit argument is clearly a big issue.

Secondly, BUSINESS CONTINUTY RISK is high. With the movement of people within the bank and outside the bank the risk from a business continuity point is high. Process and workflow based on MS Excel is not standardised which pose a huge risk when new or old manual processes are not followed.

And THIRDLY, SPREADSHEET LIMITATIONS. Although the Excel software is feature-rich and can cater to most business requirements, it is plagued with limitations. We explore some of these limitations and explain how they would impact regulatory disclosures, more specifically shareholding disclosure and flag to the users the possible risks that could blindside users that are overly reliant on Excel.

EXCEL IS NOT ABLE TO MANAGE LARGE DATASETS.

With the exponential growth of data in the last decade, Excel was not designed to handle such volume. For shareholding disclosure, position and transaction data are extensive as they contain many rows and columns of data. They often require complex calculations to aggregate positions. Excel, in particular, is not good at handling large file sizes and will be slow or unable to calculate complex calculations over a large dataset. It would not be scalable to rely on excel to both manage and calculate position data. For Shareholding Disclosure we are dealing with lots of data, plenty of complexity which poses many risks and hidden errors, detrimental to an organisation/individual.

PRONE TO MISTAKES

In the complex world of shareholding disclosure, every ‘penny’ aka decimal point counts. A slight miscalculation could mean severe penalties like fines or jail terms as demands are for accuracy. In Excel, it is easy to commit a mistake, and there is no way to validate any of the calculations other than manually checking the formula/fields. It hinders productivity as it becomes extremely time-consuming to validate each field for accuracy.

For Shareholding Disclosure that ‘one share’ could trigger a breach

MACROS

Many institutional users have tried to automate the shareholding process using macros. However for shareholding disclosure the process is notably complex – data processed is for position and transactions but lets focus just on positions first, next is the types of instruments to account for, next is ownership at entity and fund level depending on regulator.

Calculating the final position is no menial task, the difficult task of matching the data with the regulations. What one see here is a looping process as the logic requires this to be looked at in different ways.

Truth be told macros can’t be created for actions that need to be looped. The bottomline is you that can’t use Excel recorder to create/record macros for tasks that need to be looped; i.e. tasks that need to be repeated a great number of times but there lies the issue – the logic to complete SD is multiple ‘checks’ or loops before you know exactly what you need to disclose.

The Artius Global Shareholding Disclosure solution solves this issue by taking the calculations to the system and ensuring that the fields used for calculation represent the rule required for disclosure. It automates the calculation complexity and removes the possibility of human error.

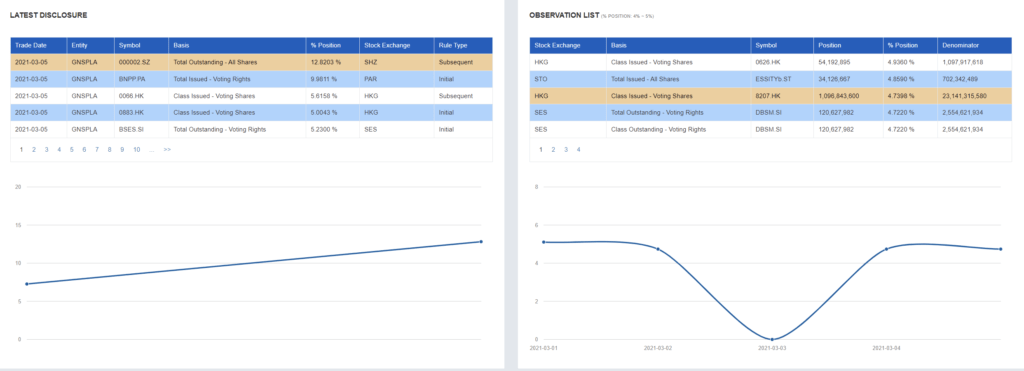

Limited Data Visualization

In Excel, data visualization is limited to static graphs and does not automatically reflect the changes when new data comes into play. The process for SD is a daily monitoring and checking process and in AGSD, we show you how to automate and show the position trends whenever new data gets uploaded into the system.

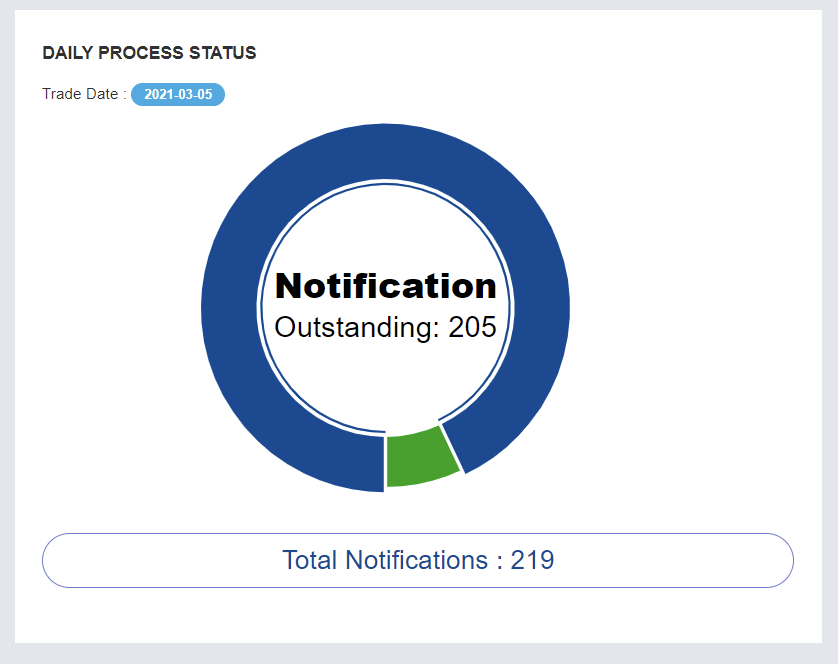

SHAREHOLDING DISCLOSURE WORKFLOW

In Excel, we will be able to calculate and see if there is a threshold breach. However, it is a process that could introduce mistakes. Calculating disclosure requirements for different markets with different formulas will be extremely time-consuming and tricky. Using AGSD, all you would have to do would be to upload the position data and let the system do all the work. You will receive notifications of any threshold breaches. Its that simple – all the logic aka macros have been built for you.

Security controls

Downloading data to a spreadsheet will result in data leakage as the data is not under security controls enacted by the company. This is especially important as financial institutes have strict data policies, and any data leakage or misuse could be detrimental to you or the company. In AGSD, data flows from upstream systems pre-approved by the security and compliance department through secured channels. We also have a detailed logging system of any changes done in AGSD.

Support of Excel vs AGSD Support

Although MS Excel is easy to pick up you are on your own, complex function could be a pain to program. There is no dedicated support from Excel to help you with your specific functions. With Artius Global we support our clients through our comprehensive support program.